The Logic of the Recognized Equivalent

Economic competition happens continuously, even in routines. The first barter exchange cannot be dated, but the form of equivalence always dictates the rules.

I want a bottle of water after a run. I have no cash and no card. The store will not accept labor as payment. My effort cannot be converted into the price of the bottle at the moment of exchange. The system recognizes only one equivalent. Without it, the transaction does not exist.

The dollar in onchain markets operates through the same logic of recognized equivalence — and that is the entire story of stablecoins.

Why Dollar Stablecoins Reinforce the Dollar Instead of Weakening It

The U.S. national debt keeps growing, yet stablecoins do not weaken the dollar. They reinforce it.

Capital that should strengthen the reserves of other states flows instead to USDT and USDC issuers — entities regulated by U.S. authorities. This creates a closed financial circuit: reserves demand Treasuries, Treasuries support the dollar, the dollar supports stablecoins, and stablecoins bypass traditional financial restrictions, feeding liquidity back into the dollar system.

For Washington’s counterparties, the result is the same regardless of intent: they continue to support the U.S. debt machine, even when they imagine themselves outside of it.

The Closed Loop: How Moscow and Beijing Read It

Moscow and Beijing see in this a mechanism of gradual, silent restructuring of U.S. external debt. Obligations move into tokens whose value adjusts flexibly. Inflation erases past commitments without official write-offs.

The U.S. has been issuing Treasuries for decades, diluting the value of each outstanding dollar. A hundred dollars in 2005 and a hundred dollars in 2025 are not the same instrument.

The Scale: Over 99% of Stablecoins Are Pegged to the Dollar

Over 99% of stablecoins in crypto are pegged to the U.S. dollar. This is not simple dominance. It is the capture of the digital economy’s monetary layer before that layer has properly formed.

Scale matters here. Stablecoins’ combined market capitalization is over $300 billion, and they already support transaction volumes measured in the tens of trillions — though, crucially, this figure includes automated transactions, meaning their usage as a normal payment method is far lower. Nonetheless, once an instrument reaches that size, questions of governance, currency power, and systemic impact become unavoidable.

Most activity sits on Ethereum and Tron, followed by rising flows on Base, Solana, Aptos, and BNB. USDT and USDC dominate; all other issuers combined account for a small remainder, and non-USD stablecoins for a fraction of a percent.

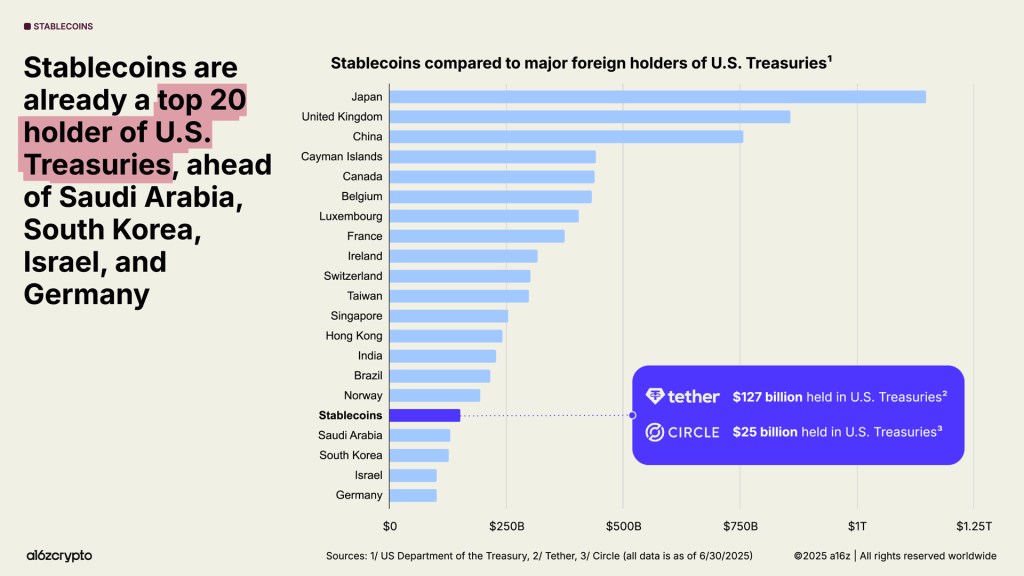

Why Stablecoin Issuers Became Major Holders of U.S. Treasuries

Stablecoin issuers have become roughly the 17th largest holder of U.S. Treasuries, up from 20th in 2024, with around $150 billion in exposure. That places them above Saudi Arabia, South Korea, Israel, and Germany. Only Japan, the U.K., and China hold more. Independent macro research, including a16z’s, has pointed to the same structural effect: stablecoins strengthen the dollar and reduce pressure on U.S. sovereign debt even as that debt increases.

| How the mechanism works | Stablecoin issuers mint tokens, then buy U.S. Treasuries as backing. This creates additional demand for U.S. sovereign debt — demand that is global, permissionless, and not limited by traditional banking restrictions. Users worldwide can acquire stablecoins even when access to dollar banking rails is blocked. |

| Why the U.S. loses nothing | Capital leaks out of the reserve systems of other countries and flows into dollar stablecoins. The debt does not disappear — it remains externalized, but now held via intermediaries regulated by U.S. agencies. External influence on issuance volumes becomes effectively impossible. Attempts by sovereign funds to reduce USD exposure are offset by the expansion of the stablecoin layer. |

| Why Russia and China call it debt softening | Debt can migrate into tokenized form, where its underlying value can be repriced under new monetary conditions. When the monetary format changes, the rules change. Old obligations can be diluted, overridden, or de facto devalued under the guise of technological progress. |

Dollar Dominance Moves from Banks to Onchain Rails

Offline, the dollar still holds around 56% of global reserves and roughly half of international settlements. Now the same dominance extends into digital infrastructure — global exchange APIs, DeFi liquidity, credit markets, bridges, and RWA platforms.

Southeast Asia, Africa, and Latin America are returning to the dollar not through banks but through crypto rails. The U.S. gains global financial presence without direct investment. The dollar becomes the default logic of the onchain world.

A Currency Needs Four Roles — Dollar Stablecoins Fill All Four

In 2025, the market was flooded with stablecoin announcements. There is nothing surprising in that. A currency remains a currency only if it fulfills four roles: unit of account, means of payment, reserve, and asset. Dollar stablecoins satisfy all four:

- Onchain pricing is denominated in USD

- Cross-border crypto payments run on USDT and USDC

- DeFi accepts the dollar as universal collateral

- RWA markets are priced in USD

Not issuing national stablecoins is not a delay. It is an exit from digital economic loops for years.

Why CBDCs Don’t Solve This

CBDCs do not close this gap. They are legally and technically closed. They function as tools of domestic monetary control, not as currencies of global digital commerce. mBridge, the BRICS bridge, and similar interbank constructions are pipes for regulated institutions. They do not create user-level liquidity. They do not create an economy around them.

Russia’s Digital Financial Assets: Useful, but Not a Currency

Against this background, the Russian logic becomes clear. The regulator is not avoiding stablecoins because it distrusts the technology. It is solving a different, primary task: giving domestic businesses fast liquidity inside a controlled framework.

That is why the Digital Financial Assets market grew in Russia — and grew specifically as a market of digital debt. These are short claims with clear maturity, yield, and simple issuance. Useful for internal corporate treasury. But they are not currencies, not settlement instruments, and not carriers of international liquidity. Digital Financial Assets do not create an onchain economy capable of competing with the dollar.

Digitalization in Russia followed a banking logic: faster borrowing, stronger oversight, higher transparency. This makes sense for the domestic market, but it leaves a vacuum at the level of digital currency — a vacuum instantly filled by the dollar via stablecoins.

National Stablecoins Are Not Imitation — They Are Re-entry

Launching national stablecoins is not an attempt to imitate the U.S. It is an attempt to re-enter the game.

While Moscow and Beijing fight dollarization in the banking sector, they are absent in the onchain sector — where P2P payments and stablecoin flows are growing around 50% annually. This absence is a strategic error. The digital economy does not tolerate empty spaces. If the ruble and yuan do not fill that layer, the dollar does.

The Cost of Staying Absent Onchain

A national stablecoin layer carries concrete advantages:

- A monetary ecosystem forms around the currency: trading, lending, market-making, RWA issuance, derivatives.

- Reduced sanctions vulnerability.

- Lower cost of international transfers.

The risks of inaction mirror them:

- The dollar returns through stablecoins.

- The yuan and ruble stay outside global SME digital trade.

- Standards and liquidity remain under U.S. control.

- Every transaction carries a hidden “dollar tax” through fees and infrastructure dependency.

What Russia and China Actually Need

Three things: national onchain infrastructure, regional financial corridors, and a fully compatible digital currency layer capable of operating in global markets.

Russia is moving cautiously — experimental regimes look more like preparation for a ruble stablecoin, though primarily as a sanctions-resilience instrument. China holds a strict line: crypto is banned, the digital yuan is the priority. But private business does not wait. Through Kyrgyzstan and Kazakhstan, ruble-backed and yuan-backed stablecoins are already being launched. The market expands aggressively.

The Window Is Closing

Falling behind in onchain economics cannot be corrected by policy statements. Only liquidity, standards, and real digital currencies correct it.

The United States is building a new global financial layer. Others act as if time still belongs to them.

It doesn’t.

FAQ

Why do dollar stablecoins strengthen the dollar instead of weakening it? — Stablecoin issuers back their tokens with U.S. Treasuries. Every dollar into USDT or USDC becomes new, permissionless demand for U.S. sovereign debt. The dollar gains reach without the U.S. spending anything.

How much of the stablecoin market is pegged to the U.S. dollar? — Over 99%. Non-dollar stablecoins are a fraction of a percent, so the monetary layer of the onchain economy is effectively a dollar layer.

What is the difference between stablecoin market cap and transaction volume? — Market cap, over $300 billion, is the value in circulation. Transaction volume, in the tens of trillions, is total movement over a period and includes automated transfers. Real payment use is far lower than the volume figure.

Do CBDCs compete with dollar stablecoins? — No. CBDCs are closed systems for domestic monetary control. They create no user-level liquidity and no global economy, so they don’t contest the dollar’s onchain position.

Why don’t Russia and China issue national stablecoins? — Both prioritized domestic control — Russia through Digital Financial Assets, China through the digital yuan and a crypto ban. Neither built a global digital currency layer, leaving the onchain settlement layer to the dollar.